Published April 22, 2026

PCS Orders and an Underwater Mortgage? Here's What VA Homeowners Need to Know

Getting PCS orders is stressful enough. When you add in the realization that selling your home might not cover what you owe on the mortgage, it can feel overwhelming — especially if you bought at the top of the market, rolled the VA funding fee into your loan, or are facing rising selling costs.

The good news: if you have a VA loan and you're being transferred, you have options. More options than most civilian homeowners in the same situation, in fact. Here's a plain-English walk through what's available, in roughly the order most homeowners should consider them.

First, Understand Why You Might Be Short

A lot of VA borrowers who bought in 2022 or 2023 are surprised to discover they'd come up short at sale even when their home's value has held steady. Here's why.

When you used your VA loan, the funding fee (typically 1.25% to 3.3% of the loan) was likely rolled into your mortgage balance. That means your starting loan amount was already higher than your purchase price. Add three years of minimum principal paydown on a 30-year loan (which is very slow in the early years) and the typical 6–8% in selling costs — agent commissions, title, transfer fees, concessions to the buyer — and the gap between what your home will sell for and what you need to pay off can easily run $20,000 to $40,000 or more.

Before doing anything else, get three numbers:

- A current payoff quote from your loan servicer

- Your interest rate from the original note

- A Comparative Market Analysis (CMA) from a local agent

Those three numbers determine which path makes the most sense.

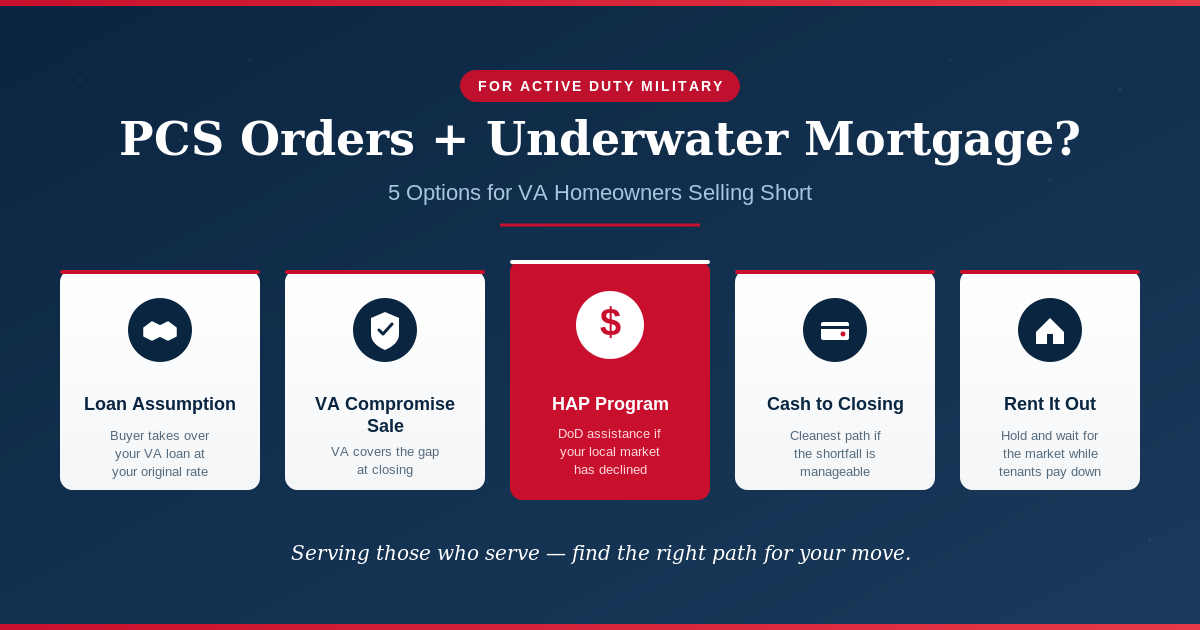

Option 1: Have a Buyer Assume Your VA Loan

If your note was signed when rates were lower — anywhere in the 5s or below — loan assumption may be your best option, and most sellers don't realize it's available.

VA loans are assumable. A qualified buyer can take over your existing mortgage at your original interest rate, with the lender's and VA's approval. In a higher-rate environment, an assumable loan with a sub-6% rate is a genuinely valuable feature that can help your home sell at or above the loan balance, closing the gap entirely.

A few things worth knowing:

- The buyer does not need to be a veteran, but if they aren't, your VA entitlement stays tied up in the home until that loan is eventually paid off.

- A VA-eligible buyer can substitute their entitlement for yours, freeing you up to use your full VA benefit at your new duty station. This is the ideal scenario.

- Assumption fees are modest — typically a 0.5% funding fee plus a lender processing fee.

If your rate is attractive, work with an agent who has marketed assumable loans before. It's a different playbook than a standard listing.

Option 2: VA Compromise Sale

When the sale price truly won't cover the mortgage and there's no other way to close the gap, the VA Compromise Sale is the program designed exactly for your situation.

Think of it as a pre-approved short sale tailored to VA-backed loans. The servicer and the VA review and approve the sale in advance. At closing, the VA pays the lender the difference between the sale proceeds and the loan balance so you don't have to bring cash to the table or carry the debt forward.

PCS orders strengthen your case significantly. The VA specifically recognizes military relocation as a qualifying hardship, which can streamline the process.

The application package generally includes:

- Your PCS orders

- A hardship letter explaining the situation

- Recent pay stubs, tax returns, and bank statements

- A listing agreement and a bona fide purchase offer

- A current CMA or appraisal

Your loan servicer handles the submission to the VA. Most servicers have a dedicated loss mitigation department that processes these requests.

Option 3: Homeowners Assistance Program (HAP)

The Department of Defense's Homeowners Assistance Program, administered by the U.S. Army Corps of Engineers, can provide direct financial assistance to service members forced to sell at a loss due to a PCS move.

HAP is real money — in some cases it can reimburse a portion of the loss, cover closing costs, or even make up the difference between sale proceeds and the loan balance. But it has a specific eligibility requirement: the local housing market must have declined meaningfully (typically measured as a 10% or greater drop in fair market value) since your purchase.

If comparable homes in your neighborhood are genuinely selling for less than you paid, submit an inquiry. If the market is flat or up and your shortfall is really driven by the funding fee and closing costs, HAP likely won't apply — but it costs nothing to ask.

Start at hap.usace.army.mil to check current eligibility windows and application requirements.

Option 4: Bring Cash to Closing

Sometimes overlooked, but worth running the math on. If the shortfall is modest and you have the liquidity to cover it, bringing cash to closing is the cleanest option:

- Zero credit impact

- VA entitlement fully preserved

- No lengthy approval process

- You walk away with a clean slate and can use your full VA benefit at the new duty station immediately

For a shortfall under $20,000, this is often the right answer for service members who have savings and want to avoid the paperwork and credit implications of a compromise sale.

Option 5: Rent It Out

If your rental market supports it, renting the home rather than selling can sidestep the shortfall entirely. VA loan terms allow you to rent the property after you've occupied it as your primary residence, which you have.

The math works if the rent covers principal, interest, taxes, insurance, HOA fees, and ideally leaves a small buffer for vacancies and repairs. The downsides are real: managing property from your next duty station, handling tenants through a management company (typically 8–10% of rent), and being on the hook for major repairs.

If you expect values to recover over a few years, this can let principal continue to pay down while you wait out the market.

What About My Credit?

A common question: does a VA Compromise Sale hurt your credit?

Yes, but generally less than most people expect and much less than a foreclosure.

The loan typically reports as "settled for less than the full balance" or similar. For a borrower with strong credit going in, the score impact is often 50–125 points. For someone already carrying some late payments, the incremental impact is smaller. The biggest driver is whether you were delinquent leading up to the sale — late payments hurt more and linger longer than the settled-status notation itself.

A few practical points:

- Some servicers require delinquency before they'll process a compromise sale. Others will work with a current borrower if the hardship is well-documented. Push back with your PCS orders before missing payments.

- The tradeline stays on your credit report for seven years, but the practical impact fades substantially after 24 months.

- For a future VA loan, there is typically a two-year seasoning period after a compromise sale. FHA typically requires three years, though PCS-related hardship can sometimes qualify for exceptions.

- Pull your credit reports from all three bureaus at 30 and 60 days after closing to verify everything is reported correctly. Errors are common and easier to fix early.

Compared to a foreclosure — which causes a much larger score drop, carries a longer seasoning period for future mortgages, and is much harder to explain to future lenders — a compromise sale is a recoverable event for most borrowers.

A Few Other Protections Worth Knowing

- Servicemembers Civil Relief Act (SCRA) provides interest rate caps and foreclosure protections while you work out a solution. It doesn't forgive a shortfall, but it can buy breathing room.

- Installation legal assistance offices provide free counsel to active duty service members and can review documents, explain your options, and help with lender communications.

- Lender-specific military relocation programs sometimes go beyond federal requirements. Ask your servicer directly whether they have one.

Putting It All Together

The right path depends on three things: your interest rate, the condition of your local market, and how much cash you have available.

- Low rate and the market is stable or up? Lead with loan assumption.

- Market has declined meaningfully? Apply for HAP while pursuing a sale.

- Shortfall is modest and you have savings? Bringing cash to closing preserves your VA entitlement and credit.

- None of the above? A VA Compromise Sale is the right tool, and PCS orders make it more straightforward than most assume.

- Strong rental market? Consider holding and renting.

Most service members don't have to choose blindly. Getting your payoff quote, your interest rate, and a local CMA in hand turns this from a stressful unknown into a clear decision.

We Can Help

If you have PCS orders and you're trying to figure out what your home can realistically sell for — and what that means for your mortgage payoff — reach out. We'll pull the comps, walk you through the math, and help you decide which path is right for your situation. There's no cost for the initial conversation, and the sooner you start planning, the more options stay on the table.

This article is for informational purposes only and does not constitute legal, tax, or financial advice. Program eligibility, benefits, and requirements change over time. Always confirm current rules with your loan servicer, the VA, the Army Corps of Engineers HAP office, and a qualified attorney or financial advisor before making decisions.