Published February 2, 2026

How to Compare Loan Estimates and Find the Best Mortgage Deal

How to Compare Loan Estimates and Find the Best Mortgage Deal

When shopping for a mortgage, many buyers focus only on the interest rate. While the rate is important, it’s only one part of the overall cost of a loan.

Different lenders structure their fees differently, and some costs shown on a Loan Estimate are controlled by the lender, while others are third-party or government fees that will be similar no matter which lender you choose.

Understanding the difference can help you compare loan offers more effectively and avoid overpaying.

Mortgage disclosures are standardized by the Consumer Financial Protection Bureau (CFPB) and explained in the

Loan Estimate.

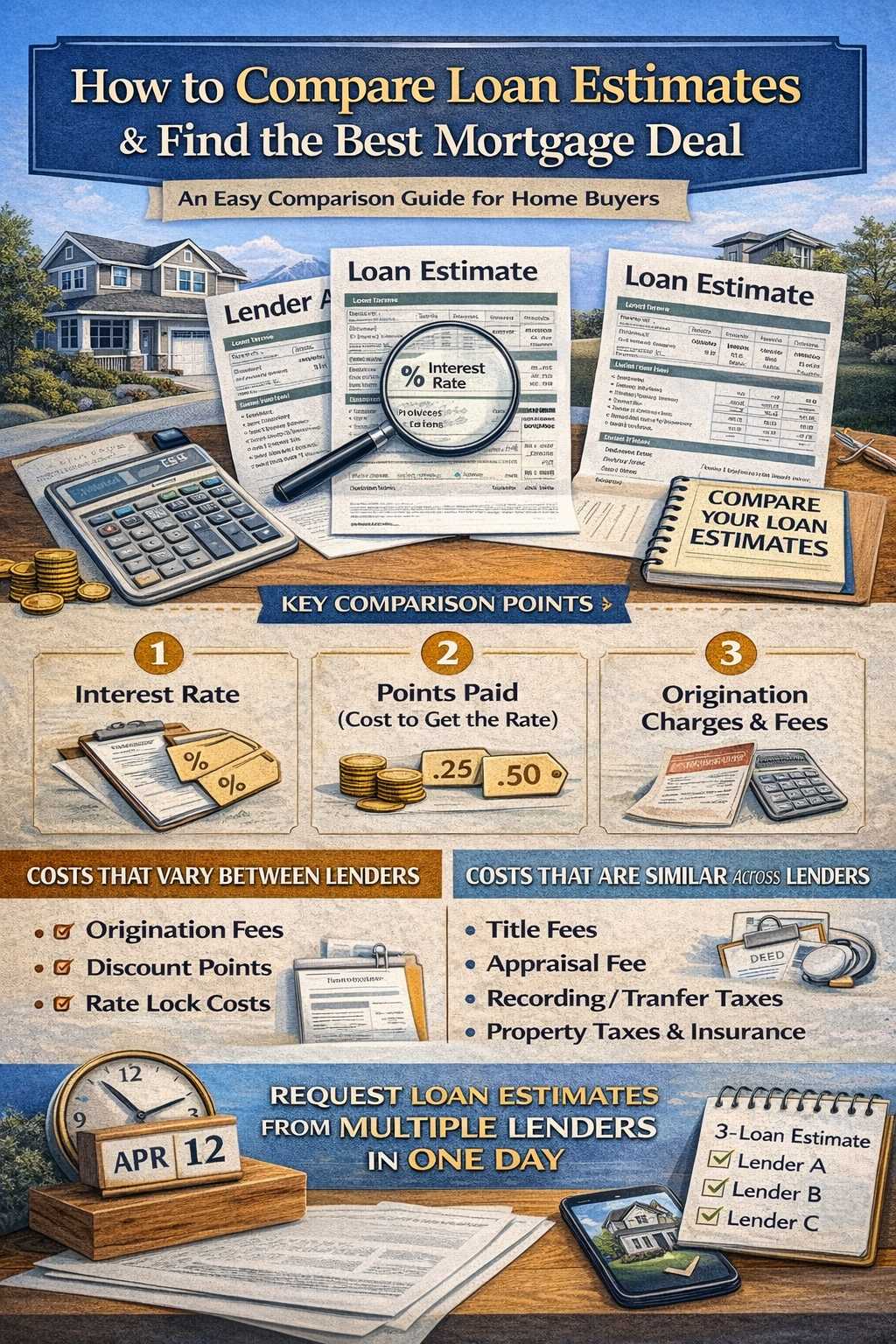

Step 1: Obtain Loan Estimates From Multiple Lenders

The best way to compare loans is to request Loan Estimates from at least two or three lenders within a short period of time.

When requesting quotes, provide each lender with the same basic information, including:

- Purchase price

- Estimated down payment

- Loan program (conventional, FHA, etc.)

- Credit score range

- Occupancy (primary residence, second home, investment)

This helps ensure you are comparing similar loan scenarios.

If possible, ask lenders to prepare estimates on the same day, since interest rates change frequently.

Step 2: Focus on the Key Areas of the Loan Estimate

Loan Estimates contain several sections, but a few areas are particularly important when comparing lenders.

Page 1: Interest Rate and Monthly Payment

This section summarizes:

- Loan amount

- Interest rate

- Estimated monthly payment

- Whether the rate is locked or floating

While a lower rate is appealing, it may come with higher upfront costs.

Page 2: Closing Costs Breakdown

This page divides costs into three main categories:

- Loan Costs (lender-related)

- Services You Cannot Shop For

- Services You Can Shop For

Understanding these categories is the key to comparing lenders effectively.

Costs That Vary Between Lenders

The most meaningful differences between lenders usually appear in Section A: Origination Charges.

These are the fees the lender controls.

Examples include:

- Loan origination fees

- Discount points

- Underwriting fees

- Processing fees

Some lenders advertise a lower interest rate but charge points or higher origination fees to offset that rate.

In other words, you may be prepaying interest upfront.

When comparing lenders, look carefully at:

- The interest rate

- The points paid

- Total origination charges

These are the true variables between loan offers.

“Pass-Through” Costs That Are Similar Across Lenders

Many costs listed on a Loan Estimate are third-party expenses.

These fees do not belong to the lender and typically remain similar regardless of which lender you choose.

Common examples include:

Title and Escrow Fees

These cover services such as:

- Title search

- Title insurance

- Escrow settlement services

These fees are usually determined by the title company, not the lender.

Government Recording Fees

Local governments charge recording fees to register:

- deeds

- deeds of trust

- mortgages

These fees are generally fixed by the county or state.

Transfer Taxes

While some areas of the country charge transfer taxes to a Buyer when property changes ownership, Washington State's real estate excise tax is paid by the Seller, and therefore should be on your loan estimate (or should not be reflected as a charge due by the buyer/borrower).

Property Taxes and Prepaid Insurance

Lenders often collect several months of:

- property taxes

- homeowners insurance

These funds go into an escrow account and are not profit for the lender.

Appraisal Fees

Most lenders require an appraisal performed by a third-party licensed appraiser.

The cost of the appraisal is typically similar regardless of lender.

Why These Pass-Through Costs Matter

Because many costs are fixed or similar across lenders, comparing total closing costs alone can be misleading.

One lender may appear cheaper simply because they estimated:

- lower property taxes

- lower insurance premiums

- lower title fees

But those costs will likely be similar regardless of lender.

The most meaningful comparison usually comes down to:

- interest rate

- discount points

- lender origination fees

Watch for Points and Rate Buydowns

A lender may offer:

- a lower interest rate with points, or

- a higher rate with fewer upfront costs

Neither option is automatically better.

The right choice depends on:

- how long you expect to keep the loan

- your available cash for closing

A common strategy is to compare loans with zero points to see the true cost of each lender’s rate. Once you know the baseline rate, you can decide if you want to increase the rate to pay your closing costs and save your cash short term, or pay points/buydown in order to lower your payment long term.

Ask for a “Same Day” Comparison

Mortgage rates can change daily. To make an accurate comparison, try to obtain loan estimates within the same day or two. Otherwise, one lender’s quote may simply reflect a different rate environment.

A Simple Way to Compare Lenders

When reviewing loan estimates, focus on three numbers:

- Interest rate

- Points paid (if any)

- Total lender fees in Section A

These are the costs most likely to vary between lenders.

Protect Your Credit and Avoid Upfront Fees During the Shopping Stage

When comparing lenders, it’s important to protect both your credit score and your cash while you are still in the loan shopping phase.

Shop Within a Short Time Window

Credit scoring models generally treat multiple mortgage inquiries made within a short window—typically about 14 to 45 days—as a single inquiry.

This allows buyers to compare offers from several lenders without significantly affecting their credit score.

To take advantage of this rule:

- Request loan estimates from multiple lenders within the same time period

- Avoid spreading applications over several weeks or months

- Try to gather quotes within a day or two if possible, since interest rates change frequently

Be Careful About Upfront Fees

While you are still comparing lenders, be cautious about paying application, underwriting, rate lock, or appraisal fees.

Some lenders request these fees early in the process, but paying them too soon can make it harder to switch lenders if you later find a better loan.

During the shopping stage, many buyers can obtain a Loan Estimate and rate quote without paying upfront fees.

Common fees you may want to delay until selecting your lender include:

- Application fees

- Underwriting or processing fees

- Rate lock fees

- Appraisal fees

Keep Your Options Open Until You Choose a Lender

The goal of the shopping stage is to compare lenders freely and choose the best loan for your situation.

By requesting loan estimates within a short timeframe and avoiding unnecessary upfront fees, buyers can:

- Protect their credit score

- Maintain flexibility to switch lenders

- Make a more confident decision about which lender to work with

Once you’ve selected the lender offering the best overall combination of rate, fees, and service, you can then move forward with locking the rate and ordering the appraisal.

Final Thoughts

Shopping for a mortgage can feel complicated, but comparing Loan Estimates becomes much easier once you understand which costs actually vary.

Remember:

- Lender-controlled costs include interest rate, points, and origination fees.

- Pass-through costs like taxes, title, recording, and appraisal fees are largely the same no matter which lender you choose.

By focusing on the true variables between lenders, buyers can make a more informed decision and potentially save thousands of dollars over the life of their loan.